Simple Mortgage Payment Calculator

Without including an estimate for taxes and insurance, the payment results would not include the escrow amount. Please get a good insurance quote from a reputable insurance professional and a tax estimate from your municipality’s taxing authority or property appraiser for the home you wish to purchase.

Simple Loan to Value Calculator

Frequently Asked Questions – FAQs

How much cash will I need (Cash-to-close)?

Answer: Cash-to-close or the amount of liquid cash needed at closing is determined by the individual loan product and your unique situation. These amounts can be quite different based in the loan type/product and if you are purchasing, re-financing, or using equity in property you already own.

The required minimum investment or down payment could be a low as 0% for VA and USDA mortgages or a high as 20%+ for those purchasing second homes or for those with less than stellar credit scores and credit history. Most FHA loans require a minimum of 3.5% down and Conventional loans require 5%, unless you are a first-time home buyer (not having owned, or been on title of a home, in the last 3 years). First-time home buyer provides an option for only 3% down. In addition to the required minimum investment there are other “costs to borrow” aka. closing costs. These may include; loan fees (origination fees, processing fees, underwriting fees, and points (pre-paid interest for a lower note rate), up front mortgage insurance premiums and funding fees, title insurance and other title fees and endorsements, appraisal fees, survey fees, inspection fees, settlement provider fees, regulatory fees (taxes imposed by local and state governments), pre-paid items such as property taxes and homeowners insurance as well as initial escrows which are several months of estimated taxes and insurance payments.

If you are purchasing an existing home, you will need to have enough cash to cover the required minimum investment/down payment, the costs to borrow and have enough reserve funds to cover your existing debt payments and the new mortgage payment for several months to qualify for a loan. Some loan products allow the home seller to credit you a portion of the purchase price to cover some of these costs.

Some loan products allow cash gifts from family members and employer assistance to cover these costs. Gifts of equity are also an option if the home or land seller is selling the property for less than market value and they are a “qualified family members or gift donors.” This would allow you to borrow against the gifted equity to help pay for the initial investment and costs to borrow. Please speak to a loan officer before arranging a gift or employer assistance as they must comply with the loan products underwriting guidelines, and the documents (gift letter, sales contract and/or purchase agreement) must contain specific language to be acceptable.

If you are purchasing a new home using a construction loan product the builder/dealer may also credit a portion of the sales price to cover some of the costs to borrow. If you are building a new home on land that you already own, the land value or equity also allows you to finance the cost to borrow and satisfy the required minimum investment provided the appraised value exceeded the loan-to-value ratio maximum. Note: land equity does not reduce the amount you are borrowing to buy/build a home, it only allows you to borrower against it to cover the cost to borrow and required minimum investment and may also lower your interest rate based on the loan to value (LTV) on most mortgage products.

Some lenders, lending products, and government agencies provide for down payment assistance (DPA) to qualified borrowers. These programs are typically reserved for lower income borrowers or those buying in specific communities identified by the government agency. You should research what DPA programs are available in your area to see if you qualify and/or ask your loan officer if there are any lender programs offered that you may qualify for.

Also note that an appraisal will determine the actual loan-to-value ratio for the purchase. The lender will only lend up to the maximum loan to value amount. Therefore, if the appraisal comes up short, you will need to bring the difference between the appraised value and the purchase price plus the cost to borrow as additional cash-to-close.

Example using a conventional loan with a maximum 95% LTV

Purchase Price: $250,000

Appraised Value: $245,000

Maximum Loan to Value: 95%

Maximum Loan Amount: $232,750 (95% of the Appraised Value)

Required Initial Investment $12,250 (5% of Appraised Value) + Appraisal Short Fall $5,000 + Cost to Borrow

What is Loan-to-Value?

Answer: Loan-to-Value (LTV) is the amount of the loan divided by the purchase price of the home. The down payment for a loan can be cash and/or land equity if you are using a new construction loan for which you already own the land where the new home will be built. Different loan products require different loan to value amounts or percentages. For example: A VA loan does not require a down payment therefore the LTV can be 100%., where as an FHA loan requires 3.5% down or 96.5% LTV, a first-time home buyer conforming conventional loan requires 3% down or 97% LTV, and 5% down or 95% LTV for a non-first-time home buyer conforming conventional loan. Other non-conforming and non-qualified loan products have different LTV requirements. Note these are the minimum required down payments and LTVs, putting more down and having a lower LTV could also reduce the note rates, lower or eliminate mortgage insurance (MIP or PMI), and increase your purchasing power/loan amount.

What is Escrow?

Answer: Escrow is a separate non-interest-bearing account in which a portion of your monthly loan payment is deposited to pay for your annual tax and homeowners insurance bills. Escrows are typically required by most lenders to ensure you do not miss these important payments that can put you and the lender at risk if they are not paid. Escrows can be waived by the lender, at their discretion, and typically when the borrower has exceptional credit and considerable equity.

What is PMI?

Answer: Private mortgage insurance. This is only on conventional loans with less than 20% equity and It protects your lender if you stop making payments on your loan.

What is MIP?

Answer: Mortgage insurance premiums. This is only on FHA loans and is no longer canceled once you reach a certain home equity percentage. If you have at least 10% down at the time of your purchase, you’ll pay MIP for 11 years. If you have less than 10% down, you’ll pay MIP for the entire term of your loan. Mortgage insurance is put into place to insure your lender against losses if you default on your loan. There are also two separate costs, one is the upfront premium which is typically 1.75% of the loan amount and the other, an annual fee of 0.45% to 1.05% of the principal balance applied monthly and added to your mortgage payments. The rate is dependent on the initial loan amount and how much you put down. If you would like to learn more about MIP and how to calculate the upfront premium and monthly premium, you can visit hud.gov and search for MIP.

What is MPI?

Answer: Mortgage Protection Insurance also known as Life Insurance. This can be purchased from a reputable life insurance agent and can be used by your beneficiary to pay off your mortgage loan if you die before it is paid off. This type of insurance is not required by lenders and is a personal decision you make to protect those who are dependent on your income to make the mortgage payment.

What is HOI?

Answer: Homeowners insurance. This may also include flood insurance if the home is in a FEMA flood zone. Most lenders require enough coverage to replace the home it its current condition in the event of a total loss.

What is a Back End or Debt to Income (DTI) ratio?

Answer: A debt to income ratio is the total of your minimum monthly debt payments that appear on your credit report divided by your total monthly gross income. If you have debt that does not report such as a personal loan or installment loan that you pay monthly that does not report to the credit bureaus, you should also add those amounts to the monthly minimum debt payments. Items that appear on your credit report that have a balance and no required payment are called differed loans, such as student loans, these should also be added to the total monthly debt and assumed to be 1% of the outstanding balance monthly (for most loan products). In addition, if you own investment property that you do not have a mortgage for and you pay taxes and insurance, or taxes and insurance is not escrowed you must add those amounts to the monthly debts. You may subtract debts that would be paid off by the new loan such as a current mortgage if you are re-financing or that you would pay off before closing the loan such as low balance loans with high payments or credit cards you would pay off in full. The difference between the current debt ratio and the maximum total debt ratio for your loan type multiplied by your gross income is the maximum payment. To calculate the new total debt ratio with the new loan, add the Principal Interest Taxes and Insurance (PITI) payment to the current debt ratio and if you are below the maximum allowed by the loan product you would qualify. If you, do not qualify you can either add more income, reduce debt, or reduce the loan amount. Refinancing other debt with higher payments or consolidating debt may also help you qualify.

What is a Front End or Housing Ratio?

Answer: A housing ratio is the principal, interest, taxes, and insurance for all real estate owned (REO) including the new loan payment divided by your gross monthly income. Some loan products have a maximum housing ratio that is lower than the total debt to income ratio.

What is a Certificate of Eligibility (COE)?

Answer: This is a Veterans Administration (VA) guaranteed loan document that shows that the veteran is eligible to use VA benefits to secure a loan and how much is available in addition to the maximum entitlement for the county where you wish to buy your new home. There is no maximum price for which a veteran can purchase a home for, but the loan amount is limited so that the entitlement must cover at least 25% of the loan amount.

When Can I Close?

Answer: Under the TILA-RESPA Integrated Disclosure or TRID rule, the Closing Disclosure (CD) must be provided to the borrower no later than three business days before the scheduled closing date. Saturday is considered a business day but not Sundays or federally recongnized holidays. This timing allows the borrower to review the final terms and costs of the loan before the closing and make any necessary arrangements or inquiries.

The TRID rule allows for the Closing Disclosure to be sent to the borrower in several ways:

-

- In Person: The CD can be provided to the borrower in person, either at the lender’s office or at another agreed-upon location.

-

- Email: If the borrower has agreed to receive electronic disclosures, the CD can be emailed to the borrower. However, the borrower must also confirm receipt of the email.

-

- Postal Mail: The CD can be sent to the borrower through traditional postal mail. The rule specifies that the CD is considered “received” by the borrower three business days after it is mailed, rather than the date it was sent.

-

- Other Electronic Methods: If the borrower has consented to receiving the CD through other electronic means, and the specific method is permissible under the Electronic Signatures in Global and National Commerce Act (E-SIGN Act), the lender may use that method.

It’s important to note that regardless of the method used to provide the CD, the borrower must have a reasonable opportunity to review the document before the closing. If any changes occur to the loan terms or costs between the time the CD is provided and the closing date, the lender may need to provide a revised CD with updated information and allow additional time for review.

The specific method of delivery and confirmation of receipt may vary depending on the lender’s policies, the borrower’s preferences, and any applicable regulations. Borrowers should communicate with their lender to ensure they understand how the Closing Disclosure will be provided and the process for confirming receipt.

What is the difference between a construction to permanent loan and a traditional mortgage?

Answer: A construction-to-permanent loan and a traditional loan (also known as a regular mortgage) are two distinct types of financing options for purchasing or building a home. Here’s an explanation of the key differences between these two types of loans:

-

- Purpose:

-

- Construction-to-Permanent Loan: This type of loan is designed to finance both the construction of a new home and its eventual conversion into a permanent mortgage. It combines the construction phase and the permanent financing into a single loan, eliminating the need for separate loans for construction and the long-term mortgage.

-

- Traditional Loan (Regular Mortgage): A traditional loan, or regular mortgage, is used solely for purchasing an already existing property, such as a house or a condominium. It does not include financing for construction or major renovations.

-

- Purpose:

-

- Loan Structure:

-

- Construction-to-Permanent Loan: In this type of loan, there are two phases—the construction phase and the permanent phase. During the construction phase, the borrower typically pays interest only on the amount disbursed for construction. Once construction is complete, the loan automatically converts into a traditional mortgage, and the borrower begins making regular monthly payments that include both principal and interest.

-

- Traditional Loan (Regular Mortgage): A regular mortgage involves a single loan with a fixed or adjustable interest rate, and the borrower starts making regular monthly payments that cover both principal and interest from the beginning of the loan term.

-

- Loan Structure:

-

- Disbursement of Funds:

-

- Construction-to-Permanent Loan: Funds are disbursed in stages (draws) during the construction phase to cover expenses as construction progresses. These draws are typically made at specific milestones, such as completing the foundation, framing, roofing, etc.

-

- Traditional Loan (Regular Mortgage): The entire loan amount is disbursed upfront to the seller of the property at the time of purchase.

-

- Disbursement of Funds:

-

- Approval Process:

-

- Construction-to-Permanent Loan: The approval process may involve more detailed scrutiny of the construction plans, budget, and timeline, along with the borrower’s creditworthiness and ability to complete the construction project.

-

- Traditional Loan (Regular Mortgage): The approval process focuses on the borrower’s credit history, income, employment stability, and the appraised value of the property being purchased.

-

- Approval Process:

-

- Interest Rates:

-

- Construction-to-Permanent Loan: Interest rates for the construction phase of this loan may be higher than those for the permanent phase, reflecting the added risks associated with construction.

-

- Traditional Loan (Regular Mortgage): Interest rates are typically determined by prevailing market rates and the borrower’s creditworthiness.

-

- Interest Rates:

-

- Loan Term:

-

- Construction-to-Permanent Loan: The construction phase of the loan usually has a shorter term, followed by the longer term of the permanent mortgage phase.

-

- Traditional Loan (Regular Mortgage): Regular mortgages have a fixed or adjustable term, commonly ranging from 15 to 30 years.

-

- Loan Term:

Both loan options have their own benefits and considerations. If you’re planning to build a new home, a construction-to-permanent loan might be more suitable, while a traditional loan is appropriate for purchasing an existing property. It’s important to carefully review the terms, interest rates, and repayment structures of both types of loans to make an informed decision based on your financial situation and homeownership goals.

Loan Types

A non-conforming loan is one that does not meet the guidelines set by Fannie Mae and Freddie Mac. These loans typically fall outside the standard loan limits or have unique characteristics that make them ineligible for purchase by government-sponsored enterprises. The most common reason a loan is considered non-conforming is that it exceeds the loan limits set by these agencies, making it a jumbo loan. Other non-conforming loans include government-backed loans like FHA, VA, and USDA loans, which follow their own specific requirements rather than those of conventional lenders.

A non-qualified mortgage (non-QM), on the other hand, does not meet the Qualified Mortgage (QM) standards established by the Consumer Financial Protection Bureau (CFPB). These standards are designed to ensure that borrowers have the ability to repay their loans, and they restrict features like interest-only payments, balloon payments, and high debt-to-income ratios. Non-QM loans are often used by borrowers with unique financial situations, such as self-employed individuals who rely on bank statements instead of tax returns to verify income. Other examples include loans with high debt-to-income ratios or those with alternative repayment structures that do not fit the standard mortgage guidelines.

The primary difference between the two is that non-conforming loans fail to meet the size or eligibility criteria of Fannie Mae and Freddie Mac, whereas non-QM loans fail to meet the CFPB’s strict affordability and repayment guidelines. A loan can be both non-conforming and non-QM, such as a jumbo loan with an interest-only repayment structure, but not all non-conforming loans are non-QM, and vice versa.

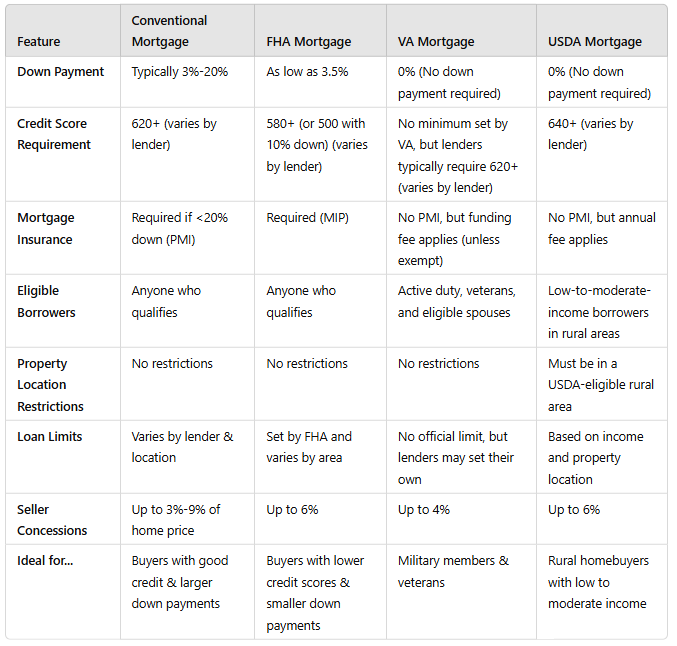

Conforming Conventional loan is a mortgage that meets the guidelines set by Fannie Mae and Freddie Mac. It has specific loan limits, borrower credit, income, and debt-to-income ratio requirements. The maximum loan amount for a single-family home in 2025 is $726,200, but it can be higher in high-cost areas. These loans typically require a down payment of 3% for first time home buyers or those that have not been on title to a home in four years to 20%. One major benefit is that conventional loans do not require an upfront mortgage insurance premium or require a funding fee. Private Mortgage Insurance (PMI) is also not required with 20% or more down payment or equity and PMI will not last for the life of the loan.

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA) that helps borrowers, particularly first-time homebuyers, qualify for financing with more flexible credit and down payment requirements. Unlike conventional loans, which often have stricter qualification criteria, FHA loans are issued by approved lenders but backed by the government. This reduces the lender’s risk and makes it easier for borrowers with lower credit scores or limited savings to secure a home loan.

One of the key advantages of an FHA loan is the low down payment requirement. Borrowers with a credit score of 580 or higher can qualify with just 3.5% down, while those with scores between 500 and 579 may still be eligible but would need to put down at least 10%. FHA loans also have more lenient credit score requirements than conventional loans, making homeownership more accessible. However, some lenders impose additional requirements, known as overlays, which may require a higher credit score than the FHA’s official guidelines. For example, while the FHA may accept a 580 score, a lender might set their own minimum at 620 or higher.

FHA loans also allow for a higher debt-to-income (DTI) ratio compared to conventional loans. In 2024, the standard maximum DTI ratio for an FHA loan is 43% of the borrower’s gross income. However, in some cases, borrowers with strong credit scores and additional financial compensating factors may qualify with a DTI ratio as high as 50% to 56.99%. This flexibility makes FHA loans appealing to borrowers with existing debt obligations.

Despite their benefits, FHA loans come with additional costs and restrictions. Mortgage insurance premiums (MIP) are required both upfront and annually, adding to the overall cost of the loan. The home being purchased must also meet specific safety and livability standards set by the FHA, which could limit options for buyers considering properties in need of major repairs. Additionally, FHA loan limits vary by county and may not be sufficient for higher-cost housing markets.

For borrowers who might not meet conventional loan requirements, an FHA loan can provide a path to homeownership. If you need help determining whether an FHA loan is the right choice for you or want assistance comparing lender-specific requirements, We can guide you through the process.

A VA loan is a mortgage option backed by the U.S. Department of Veterans Affairs, designed to help veterans, active-duty service members, and certain military spouses purchase, build, or refinance a home. One of its biggest advantages is that it usually requires no down payment, making homeownership more accessible. Unlike conventional loans, VA loans do not require private mortgage insurance (PMI), which can result in significant cost savings. They also offer competitive interest rates and have more lenient credit requirements, making them a great option for borrowers who might not qualify for traditional loans. Additionally, the VA limits certain closing costs and provides financial assistance to borrowers who may struggle to make payments. Eligibility is typically extended to veterans, active-duty personnel, certain National Guard and Reserve members, and surviving spouses of those who died in service or due to a service-related disability.

A key benefit of VA loans is the 25% loan guarantee provided by the Department of Veterans Affairs. This means the VA will cover the lender for 25% of the loan amount in case of default, which allows lenders to offer favorable terms, such as no down payment and no private mortgage insurance (PMI). This loan guarantee reduces the lender’s risk, making it easier for qualified borrowers to secure financing. There are two types of VA entitlement: basic entitlement and bonus (or second-tier) entitlement. The basic entitlement is typically $36,000, which means the VA will cover 25% of a loan up to $144,000. However, since most homes cost more than this, the bonus entitlement applies to higher loan amounts.

For loans exceeding $144,000, the VA guarantees 25% of the conforming loan limit set by the Federal Housing Finance Agency (FHFA). In most areas, the conforming loan limit is $766,550 for 2024, meaning the VA will guarantee up to $191,637.50 (25% of $766,550). In high-cost areas, the loan limit can be higher, and the VA entitlement adjusts accordingly.

To qualify for a VA loan, you must meet specific eligibility requirements related to your military service, creditworthiness, and property guidelines.

First, you need to meet the military service requirements. Active-duty service members must have served at least 90 continuous days. Veterans must have served at least 90 days during wartime or 181 days during peacetime and must have been honorably discharged. Members of the National Guard and Reserves must have completed at least six years of service unless they were called to active duty under Title 10 orders, in which case 90 days of active service may qualify them. Surviving spouses of service members who died in service or as a result of a service-related disability may also be eligible.

In addition to service requirements, you must obtain a Certificate of Eligibility (COE), which confirms your eligibility for a VA loan and the amount avaialble of your basic entitlement.. You can apply for a COE through the VA eBenefits portal, request it through us, or apply by mail.

Lenders also assess financial qualifications such as credit score and income. While the VA does not set a minimum credit score requirement, most lenders prefer a score of at least 580 to 620. They also evaluate your debt-to-income ratio (DTI), which compares your monthly debt payments to your income. A lower DTI increases your chances of approval. Additionally, lenders require proof of stable income to ensure you can afford the loan payments.

Lastly, the property being purchased must meet VA appraisal guidelines, ensuring it is safe, sound, and sanitary. The home must be your primary residence, meaning VA loans cannot be used for investment properties or vacation homes.

A USDA loan is a mortgage backed by the U.S. Department of Agriculture that helps low- to moderate-income homebuyers purchase homes in eligible rural and suburban areas. These loans offer benefits such as zero down payment, competitive interest rates, and reduced mortgage insurance costs, making homeownership more affordable for those who may not qualify for conventional loans. Borrowers must meet income and credit requirements, and the property must be located in a USDA-designated eligible area. The program includes guaranteed loans, which are issued by approved lenders and backed by the USDA to reduce risk for lenders and make financing more accessible for buyers.

A Chattel loan or Home Only loan is a type of financing used for movable personal property, known as chattel. Unlike a traditional mortgage, which is secured by real estate, a chattel loan is backed by the asset itself. If the borrower defaults, the lender can repossess the property.

These loans typically have higher interest rates than mortgages because the risk is greater due to the mobility of the asset. They also tend to have shorter repayment terms. Chattel loans are commonly used to finance items such as manufactured homes, mobile homes, boats, RVs, heavy equipment, and airplanes.

For example, if someone purchases a manufactured home that is not placed on permanent land, they might use a chattel loan instead of a mortgage. Similarly, a business acquiring construction equipment may finance it through a chattel loan rather than a traditional business loan.

A Reverse Mortgage is a type of loan available to homeowners, typically aged 62 or older, that allows them to convert part of their home’s equity into cash without having to sell the home or make monthly mortgage payments. Instead of the borrower making payments to a lender, the lender makes payments to the borrower, either in a lump sum, monthly installments, or as a line of credit. The loan balance increases over time as interest and fees accrue, and repayment is usually required when the homeowner sells the house, moves out permanently, or passes away. Reverse mortgages are most commonly issued as Home Equity Conversion Mortgages (HECMs), which are insured by the Federal Housing Administration (FHA) and come with specific regulations and protections. In addition to tapping into home equity, a reverse mortgage can also be used to purchase a home through a HECM for Purchase (H4P), which allows seniors to buy a new primary residence using a combination of their own funds and a reverse mortgage, helping them secure a home that better suits their needs without the burden of monthly mortgage payments. While reverse mortgages can provide financial relief for retirees, they should be carefully considered, as they can reduce the homeowner’s equity and may impact inheritance plans for heirs.

A DSCR (Debt Service Coverage Ratio) loan is a type of real estate investment loan that assesses the income-generating potential of a property rather than the borrower’s personal income. Instead of requiring tax returns, W-2s, or pay stubs, lenders determine eligibility based on whether the property’s rental income is sufficient to cover the loan’s debt obligations, including mortgage payments, taxes, and insurance.

To calculate DSCR, lenders use the formula: Net Operating Income (NOI) ÷ Total Debt Service. The net operating income represents the rental income after operating expenses, while the total debt service includes mortgage payments and other property-related costs. A DSCR of 1.0 means the property generates just enough income to cover the loan payments, while most lenders prefer a ratio of 1.2 or higher for approval. Some may accept lower ratios in exchange for higher interest rates or larger down payments.

This type of loan is beneficial for real estate investors, particularly those who are self-employed or have complex financial situations, because it eliminates the need for personal income verification. DSCR loans offer a faster approval process and allow investors to qualify for multiple properties based on their rental income. They are commonly used for rental homes, multifamily properties, and short-term rentals.

An Alternate Credit Loan or Alternate Income Loan is a type of mortgage or personal loan designed for borrowers who may not qualify through traditional means due to a lack of conventional credit history or standard income documentation. These loans are particularly useful for self-employed individuals, gig workers, retirees, or anyone with non-traditional income sources. Instead of relying solely on a credit score, lenders may consider alternative payment histories such as rent, utility bills, and insurance payments. Similarly, rather than requiring W-2s or tax returns, they may accept bank statements, profit-and-loss statements, or other financial documents as proof of income. Because of the perceived higher risk, these loans often come with slightly higher interest rates than conventional loans. They provide a more flexible qualification process, making them a viable option for freelancers, entrepreneurs, or investors. Some common variations of these loans include bank statement loans, no-doc or low-doc loans, DSCR (Debt Service Coverage Ratio) loans for real estate investors, and stated income loans, though the latter has become less common due to stricter financial regulations.

Conforming Qualified Mortgage Comparison